Economists ShockedEconomists were shocked by the plunge in the Conference Board

Consumer Confidence Index this morning, well below any economist's guess in

Bloomberg's Econoday Forecast.

The consensus estimate was 99.6. The consensus range was 97.0 to 102.0. And the actual result ... 90.9.

Consumer confidence has weakened substantially this month, to 90.9 which is more than 6 points below Econoday's low estimate. Weakness is centered in the expectations component which is down nearly 13 points to 79.9 and reflects sudden pessimism in the jobs outlook where an unusually large percentage, at 20 percent even, see fewer jobs opening up six months from now.

A striking negative in the report is a drop in buying plans for autos which confirms weakness elsewhere in the report. Inflation expectations are steady at 5.1 percent which is soft for this reading.

Survey MethodologyHow many people does the conference board survey each month? The answer is 3,000. Supposedly that's all it takes to determine car sales, job prospects, economic slowing, home purchases, etc.

Bloomberg reports "

While the level of consumer confidence is associated with consumer spending, the two do not move in tandem each and every month."

I will return to that idea in a bit. But first let's take a look at what others say.

Risk for the EconomyPlease consider

Plunge in Consumer Confidence Exposes Risk for U.S. Economy.

“

A less optimistic outlook for the labor market, and perhaps the uncertainty and volatility in financial markets prompted by the situation in Greece and China, appears to have shaken consumers’ confidence,” Lynn Franco, director of economic indicators at the Conference Board, said in a statement.

Really? US consumers care about the Chinese stock market and Greece? Since when?

"

A drop in U.S. sentiment this month that results in weaker retail spending would represent a challenge to the Fed," said the article.

Other Measures of SentimentThe Conference Board "

Consumer Confidence" report is not to be confused with the University of Michigan "

Consumer Sentiment" report or the Gallup "

Confidence Index" survey.

With that confusion out of the way, and in reference to the University of Michigan sentiment numbers, please consider the July 17 MarketWatch report

Consumer Sentiment Drops from Five-Month High.

Consumers’ attitudes soured in July, with a gauge of their sentiment pulling back from June’s five-month high, according to reports on the University of Michigan gauge released Friday.

The University of Michigan’s gauge of consumer sentiment fell to a preliminary July reading of 93.3 from a final June level of 96.1. Economists polled by MarketWatch had expected a July figure of 95.

Economists follow readings on confidence to look for clues about consumer spending, the backbone of the economy. Earlier this week the government reported retail sales fell in June, the first drop in four months. Americans spent less at car dealers, and furniture and clothing stores, among other areas.

However, the retail-spending drop may be short-lived, economists say. A growing economy that’s adding a healthy number of jobs should boost confidence and support spending.

”Despite the decline, consumer sentiment remains relatively high, reflective of continued improvement in job market conditions, limited inflation, and an economy that appears to have re-gathered some momentum after stumbling out of the gate early this year,” said Jim Baird, chief investment officer for Plante Moran Financial Advisors. “Recent stock market volatility, increasing gas prices, and the most recent tensions around the ongoing debt crisis in Greece were likely the key drivers of the drop."

Proposed Survey QuestionMarketWatch repeats nonsense about Greece once again.

I suggest a survey question: "

Do you give a rat's ass about Greece?"

Whether or not Greece or Italy

eventually matters is irrelevant. Until they do matter, US consumers will not care one iota.

Gallup Confidence Index Continues SlideIn contrast to the Conference Board and University of Michigan volatility, the

Gallup Confidence Index has been trending lower most of the year.

Gallup's Economic Confidence Index is the average of two components: how Americans rate the current economy and whether they feel the economy is getting better or getting worse. The index has a theoretical maximum of +100, if all Americans rate the economy as excellent or good and improving; and a theoretical minimum of -100, if all Americans rate the economy as poor and getting worse.

The current conditions score fell four points from the week prior to its current score of -9, accounting for the entire decline in the overall index. This was the result of 23% of Americans saying the economy is "excellent" or "good" and 32% saying it is "poor." Meanwhile, 39% of Americans said the economy is "getting better," while 57% said it is "getting worse." This resulted in an economic outlook score of -18, unchanged from the previous week.

Bottom Line

Though Americans' confidence in the national economy has skewed negative for six months now, the recent drop of the current conditions component comes on the heels of a new path for solving the Greek debt crisis and amid a tumultuous period for Chinese stocks. The instability abroad could be fueling Americans' doubts about the health of the U.S. economy, not to mention that the Dow closed lower several days in a row last week.

Another Blame on GreeceThere you have it: Another blame on Greece and China with the addition of the DOW dropping last week.

Might I point out to Gallup ....

- The Gallup Index has been sinking since mid-January

- The Plunge in China started in mid-June

- The plunge in the DOW (that no one really follows anyway) is essentially nonexistent

Rather than asking, analysts leap to what I believe are absurd conclusions about Greece. Why don't they just ask: "

Do you give a rat's ass about Greece?"

Poll Discrepancy Note the discrepancy in the three polls. Supposedly all these surveys are statistically valid measures of sentiment.

It seems the polls forgot to measure the same 3,000 people.

Retail SpendingLet's return to the notion that confidence equates to retail spending. Bloomberg Econoday states "

Typically retail sales will move in tandem with consumer optimism - although not necessarily each and every month."

This notion is widely believed, even by the Fed. I have questioned this belief before, but let's put the idea under the microscope for further examination.

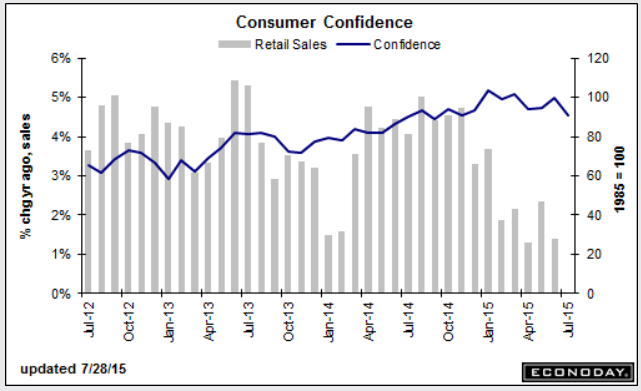

Consumer Confidence vs. Retail Sales

Unfortunately, that data only goes back to 2012 (without paying for it). But the chart, as shown, ought to raise some eyebrows on widely believed theory.

The next set of charts is even more interesting.

University of Michigan Sentiment vs. Retail Sales

That chart is certainly amusing. It suggests retail sales go up except in recessions, and perhaps even in recession. But let's look at this still one more way.

Year-Over-Year Percentage Changes: Sentiment vs. Retail Sales

Same Chart with Discrepancies Noted

Random Noise on Leading Indicators

Random Noise on Leading IndicatorsThe above chart shows year-over-year percentage changes in sentiment vs. retail sales.

The result: random noise.

Note that retail sales are not adjusted for CPI or for population growth (putting an upward pressure on sales). Nor do economists factor in demographics of aging boomers or changing attitudes of millennials (putting downward pressures on sales).

Some attitudes are fleeting, others not. And debt remains a huge overhang.

Expecting retail sales to match sentiment is a hopeless proposition, yet one economists cling to.

Supposedly, sentiment is a "leading indicator".

A leading indicator of what?

Mish Economic Prognosis - Retail spending does not follow sentiment in any predictable pattern.

- Sentiment measures often conflict.

- Sentiment is not a valid leading economic indicator.

- Consumers are not concerned about Greece.

- Consumers are concerned about rising rent.

- Consumers are also concerned about rising health care costs.

- The decline in gas prices that economists erroneously expect consumers to spend on junk, pales in comparison to points 5-6.

- A decline in auto sales, long overdue, will shock economists and the Fed.

- Rising minimum wages will take a huge bite out of job growth.

- This economy is much weaker than most assume.

I believe points 1-3 are proven. Points 4-10 are my suggestions.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com